June 2019

Cleveland Jewish News

Americans Are Better Off Now Than Ever Before

Bad news sells. Humans are hard-wired to focus more on negativity and bad news than on positivity and good news. Psychologists call this phenomenon “negativity bias.” It’s no wonder many feel the world is getting worse with the onslaught of negative media and a 24/7 news cycle.

Focusing on Danger and Doom Doesn’t Serve Us in Modern Times

According to Laura Mixon Camacho, Ph.D., a communication coach at Mixonian Institute, “The human brain remembers negative messages, results, and possibilities with greater magnitude than positive ones.” In pre-historic times, remaining alert for potential danger was the key to surviving. But, she says, “Modern times favor humans who not only imagine a better future but who put in the work to make it become reality. Fixating on negative possibilities creates harmful stress that actually shortens lifespans.”

Bad news has always dominated the headlines. In fact, publications that are launched specifically for the purpose of reporting only good news don’t stay in business long. Back in 2014, a Russian newspaper called The City Reporter published only positive news for an entire day. The result? The paper lost two-thirds of its readership that day.

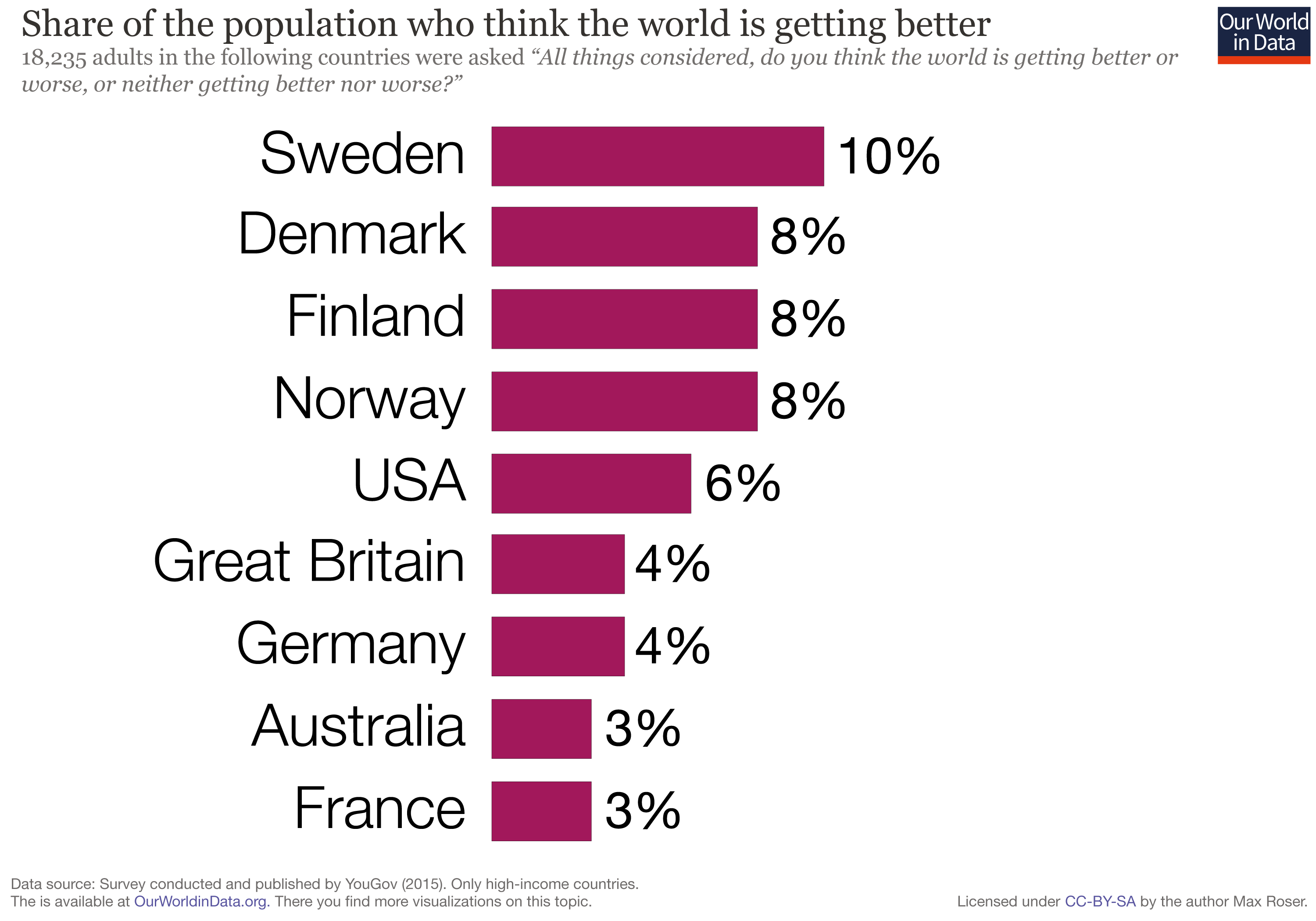

Given the onslaught of negative information, people see the world and the future as much bleaker than they really are. A recent survey asked people all over the world, “All things considered, do you think the world is getting better or worse?” In the United States, only 6 percent of the survey respondents thought things are getting better. The Swedish were a little more optimistic, at 10 percent, and only 3 percent of the French thought things were improving—of course, if you live in France they may be right.

Despite the media’s focus on gloom and doom, the average person in the United States is better off than ever before, as are people around the world generally.

A Harvard Professor Advises Us to Notice the Good Around Us

Steven Pinker, a cognitive psychologist and professor at Harvard University, agrees that there is a journalistic bias toward publishing negative news. He says negative events tend to happen suddenly. “Wars break out, terrorists attack, rampage shootings occur, whereas a lot of the things that make us better off creep up by stealth” so we are not as aware of them.

In a powerful study entitled “The short history of global living conditions and why it matters that we know it” by Max Roser, an economist at the University of Oxford, we learn that on virtually all of the key dimensions of human material well-being—poverty, literacy, health, freedom, and education—the world is an extraordinarily better place than ever before.

In the early 1980s, more than 40 percent of all humans were living in extreme poverty. Now fewer than 10 percent are.

Whereas 36 percent of the world’s population was literate in 1950, by 2010 that had jumped to 83 percent (Roser & Ortiz-Ospina, 2018b).

Life expectancy has risen 20 years over the last half century.

In the New York Times, Nicholas Kristof declared that by many measures, “2017 was the best year in the history of humanity”, with falling global inequality, child mortality roughly half what it had been as recently as 1990, and 300,000 more people gaining access to electricity each day.

By most objective measures the economy, and quality of life, for Americans is better than ever before.

Negative Headlines Hide the Truth

While the media in general, and especially political pundits, continue to discuss the negative impact of tariffs, potential trade wars, that the markets are too high, we will have a recession and other seeming bad things the facts tell another story. We have one of the best economies in the world and have one some of the strongest economic numbers in American history right now.

According to NPR, “The unemployment rate dropped to 3.6% — the lowest in nearly 50 years.” Participation is higher now than it was in the late 1960s when 3.6% was considered full employment. And that’s in spite of an aging population.

The unemployment rate for those with less than a high school degree has averaged 5.6% in the past twelve months, the lowest on record, and well below the previous cycle low of 6.3% reached during the internet boom two decades ago.

The Hispanic unemployment rate has averaged 4.6% in the past year, while the Black unemployment rate has averaged 6.4%, both also record lows.

Meanwhile, wage growth has accelerated. Average hourly earnings are up 3.2% from a year ago. And the gains in wages are not just tilted toward the rich. Among full-time workers age 25+, usual weekly earnings are up 3.5% for those in the middle of the income spectrum. But wages are up 4.9% for workers at the bottom 10% of earners, while up 1.7% for those at the top 10% of income earners. A rising tide is lifting all boats.

Nominal GDP (real growth plus inflation) is still up 4.8% at an annual rate in the past two years, and is set to equal, or exceed, that in the year ahead.

Meanwhile, the stock market has jumped 27 percent since the 2016 election amid a surge in corporate profits and as a result of corporate tax cuts and regulation.

Focusing too much on the negative can lead to decisions that may hurt us in the long run and could cause unnecessary stress. We cannot time markets or predict short-term events from terrorism, the weather or politics, nor should we try. Our team has developed and refined an investment and planning process. It takes into consideration both the expected and unexpected while being guided by your specific needs, objectives and personal vision. What the markets and economy do in the short run should not impact you.

People often ask the question of “what’s going to happen?” That may be the wrong question. The question should be “How will what’s happening impact me?” If the answer is that it won’t, then there should be no point in worrying about it. In my opinion, we are living in one of the best times and should enjoy this. Our team is here to help sift through all of the noise and help you live a happier and healthier life driven by intention, not circumstance. We call this Persona Visional Planning® and look forward to helping you live the life you have dreamed of.

Feel free to contact Randy Carver personally, or the Carver Financial Services Inc. team at randy.carver@raymondjames.com or (440) 974-0808. Carver Financial Services has served clients globally since 1990 and manages more than $1.25 Billion for clients today. There is neither a cost nor obligation to speak with an advisor.

This information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of the professionals at Carver Financial Services, Inc., and not necessarily those of Raymond James. Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members.

10,000 Square Foot Expansion Begins

MENTOR, Ohio, June 12, 2019 — The 10,000 Sq. Ft. Carver Financial Services Inc. expansion has begun at our Center Street location in the heart of Mentor.

?This expansion is part of our continuing commitment to provide our clients, team and community with a comfortable state-of-the-art building,? says Randy Carver, President of Carver Financial Services Inc., an independent practice, and Branch Manager with Raymond James Financial Services. The expansion will double the existing building size and is expected to be complete by the end of October.

In 2012, we began a planned five-phase improvement program for the building and behind-the-scenes infrastructure. Phases 1 through 4 are now complete.

- Phases 1 and 2 were undertaken and completed in 2012. This involved the complete renovation of computer systems and an update to the file center and basement conference center. This work also involved the complete demolition and remodeling of the second floor on the east side of the building. This upgrade allowed for an update to wiring, network and data technology while adding seven office spaces.

- Phase 3 involved the renovation of the reception area and exterior of the east side of the building. The new exterior is an energy-efficient exterior insulation and finish systems (EIFS) system. This phase of the project also entailed adding new servers and digital infrastructure for the building. Both handicapped accessibility and general access were improved, and parking was expanded.

- Phase 4 was the largest part of the project and was completed in October 2013. In this phase, the original one-story building was demolished and replaced with a state-of-the-art two-story facility.

“We appreciate everyone’s patience and understanding as we complete these improvements,” commented Carver. “As with our financial planning strategy, we want to be proactive with our facilities so we can continue to provide exceptional service and a great experience to our clients, and future generations, for decades to come!”

Since 1990, Carver Financial Services Inc. has been helping clients in Lake County and around the world enhance and maintain their standard of living while simplifying their lives. Randy Carver and his team manage more than $1.4 billion in assets, providing comprehensive financial planning with a focus on retirement income.

Not an Investment Brokerage – Something Different

Bill Graham, the legendary concert promoter, wrote about the Grateful Dead, “They are not the best at what they do; they are the only ones who do what they do.”

Here at Carver Financial Services Inc., that’s what we strive to do – provide a service that’s as unique as our clients. We provide Personal Vision Planning® and work to improve your life; we are not here to sell or manage investments. When you hire us, you are not hiring an investment broker or fund manager. Our goal is to improve your life and enable you to enhance and maintain your lifestyle while being confident in your future. The value of working with our team is not in beating a random benchmark such as the S&P 500. Success, in our opinion, is measured by your being able to confidently live your life the way you want to. We are here to make you and your family happier.

The Value of a Broader View of Your Well-Being

The value we provide is not reflected only in the return on your portfolio. Our team can help you reduce income tax, fund education expenses efficiently, help facilitate real estate or vehicle purchase as well as a myriad of other strategies that put more money in your pocket. Yet these valuable benefits are not reflected in a portfolio return.

Personal Vision Planning is more than just managing money; it focuses on making you happier and more comfortable. This might involve working with your CPA, attorney, insurance agent, medical professionals and others. Our firm works with integrity, transparency and discretion to coordinate your life. Our clients do not hire us solely as investment managers.

Even from a pure portfolio-return standpoint, industry studies estimate that professional financial advice can add between 3 and 4 percent to portfolio returns over the long-term, depending on the time period and how returns are calculated.[1]

The process we have developed and refined includes defining your goals, understanding your current situation and identifying the key steps to move forward. Although many firms talk about personal or customized approaches, they use standard models for their clients, do not take a holistic approach, and are focused more on investment management rather than on your life. Beyond long-term goals like retirement, and shorter-term goals like buying a house, funding your kids’ education or traveling, our process looks at factors such as legacy planning, family support, health care, insurance coverage and charitable giving.

Our Team Will Serve You for the Long Term

Our large, experienced team is composed of several generations of advisors who will be here to serve you for generations to come. We work around your schedule to accommodate your busy life. As many firms move to cookie-cutter models, reducing staff and relying on technology rather than personal contact, we have continued to grow our team of highly educated and experienced financial professionals.

We host events throughout the year that are fun, educational and inspiring. We invite you to check out the full list of our upcoming events.

Our firm was founded in 1990 with the mission of Making People’s Lives Better—Our Clients, Our Team and Our Community. We look forward to hearing from you regarding how we can best fulfill that mission for you and our community. Feel free to contact me personally at randy.carver@raymondjames.com or anyone on our team at (440) 974-0808. We are the only ones who do what we do in the financial-planning field, because we are focused not just on your portfolio return, but on enhancing your life and legacy.

[1]. Value of advice sources: Envestnet, Capital Sigma: The Return on Advice Opens (estimates advisor value-add at an average of 3 percent per year), 2016; Russell Investments, 2017 Value of a Financial Advisor Update (estimates value-add at more than 4 percent per year); Vanguard, Putting a Value on Your Value: Quantifying Vanguard Advisor’s Alpha®, 2016, (estimates lifetime value-add at an average of 3 percent); Morningstar Investment Management, The Value of a Gamma-Efficient Portfolio, 2017.

Randy Carver Named to 2019 Financial Times Top 400 Financial Advisers

April 25, 2019 – Randy Carver, RJFS Registered Principal, and the President of Carver Financial Services Inc. was once again named to the 2019 Financial Times list of Top 400 Financial Advisers.

The FT 400 was developed in collaboration with Ignites Research, a subsidiary of the FT that provides specialized content on asset management. To qualify for the list, advisers had to have 10 years of experience and at least $300 million in assets under management (AUM) and no more than 60% of the AUM with institutional clients. The FT reaches out to some of the largest brokerages in the U.S. and asks them to provide a list of advisors who meet the minimum criteria outlined above. These advisors are then invited to apply for the ranking. Only advisors who submit an online application can be considered for the ranking.

In 2019, roughly 960 applications were received and 400 were selected to the final list (41.7%). The 400 qualified advisers were then scored on six attributes: AUM, AUM growth rate, compliance record, years of experience, industry certifications, and online accessibility. AUM is the top factor, accounting for roughly 60-70 percent of the applicant’s score. Additionally, to provide a diversity of advisors, the FT placed a cap on the number of advisors from any one state that’s roughly correlated to the distribution of millionaires across the U.S. The ranking may not be representative of any one client’s experience, is not an endorsement, and is not indicative of advisor’s future performance.

Neither Raymond James nor any of its Financial Advisors pay a fee in exchange for this award/rating. The FT is not affiliated with Raymond James.

Capitalism Isn’t Fair – That’s Why it Works

As we head into the 2020 election season, we are once again hearing the cry to move away from capitalism to socialism in the United States. The idea of free health care, free education and free basic income for all is compelling and presented as fair, whereas capitalism is presented as unfair and even racist. Speaking on March 15th, 2019, former Texas congressman and Democratic candidate for president Beto O’Rourke stated, “It is clearly an imperfect, unfair, unjust and racist capitalist economy.”

A Fuzzy Understanding of Socialism and Its Implications

There is an increased interest in socialism, especially among younger people. A national Reason-Rupe survey found that 53 percent of 18- to 29-year-olds view socialism favorably, compared to only one-quarter of Americans over 55. At the same time, however, millennials don’t like the idea of the government running things, so it’s clear that they may not understand what socialism is, or what the implications are.

The promise of universal basic income (UBI), a social policy that guarantees a fixed, unconditional income from the government for everyone, free college tuition and free health care are all very appealing, especially to many younger Americans. Yet while many Americans find the socialist policy appealing, they don’t understand what the implications are. Kate S. Rourke, in her article “You Owe Me: Examining a Generation of Entitlement,” writes that there is a sense that the government will provide these “free lunches” without any true sense of how they will get paid, other than “The rich must pay.”

So what do millennials think socialism is? In the Reason-Rupe survey mentioned above, respondents were asked to use their own words to describe socialism. Millennials who viewed socialism favorably were more likely to think of it as just people being kind or “being together,” as one millennial put it. Others thought of socialism as just a more generous social safety net. Some thought it referred to social media like Twitter and Facebook!

Americans’ often fuzzy understanding of socialism can skew research results. A Harvard study revealed millennials’ apparent disregard for capitalism and favorable attitude toward socialism. However, the article acknowledged, “It is more likely that the results are less a repudiation of capitalism and more a rejection of the ‘status quo,’ which is a strange mix of cronyism, capitalism and socialism.”

In the study, millennials did not indicate support for capitalism but said they do not view the government as a solution, either. Only 27 percent answered that they believed the government should do more to regulate the economy, and only 26 percent responded that government spending can increase economic growth.

Someone Has to Pay for All the Freebies

First and foremost, “free” isn’t really free. To pay for socialist programs and policies, taxes must increase dramatically, which can take away the incentive for businesses to hire people and grow. Conversely, we have seen that lowering income taxes and reducing regulation leads to more jobs for everyone.

In the United States, as of March 2019, we have some of the lowest unemployment rates in our history and in the world. According to October 2018 figures from the International Monetary Fund, the unemployment rate in the United States was 3.5 percent, compared to much higher rates in socialist countries: Greece at 18.1 percent, France at 8.5 percent and Venezuela at 38 percent.

Proposals to fund free education, free health care and UBI in the United states range from returning income tax rates to pre-1982 levels, adding a Value Added Tax or National Sales tax (in the UK, this is 20 percent) and adding a tax to all securities transactions. All of these moves will increase the cost of goods and services to everyone and can reduce the growth of our economy.

Making decisions based on perception, or misinformation, rather than facts can lead to actions that fail to meet our needs and objectives or are harmful to our future. Seeking instant gratification and the easy path is often at the expense of our long-term well-being.

Policies that provide so-called free college, free wages and free health care are not free and will negatively impact all us in the long-run — most of all, young people. As with many things, the people these benefits are supposed to help are the ones who will be hurt the most. Aside from the psychological impact of never really accomplishing anything, these policies can make our economy suffer and even fail, as evidenced by countries that have enacted socialist policy.

“Free” Higher Education Isn’t Free

In the 2016 election, Bernie Sanders made free higher education a cornerstone of his presidential campaign, helping him get to a 54 percent favorability rating among 18- to 29-year-olds, according to a Harvard poll. Introducing the bill in a press conference, Sanders said the United States is falling behind as a world leader in educating young people. He might not be wrong about that. Moreover, the sentiment that “Our job — if we are smart — is to make it easier for people to get the education they need, not harder,” is a good one, in our opinion.

How we accomplish this, however, is a matter for discussion. Creating incentives for people to develop a skill and for private business to support this goal makes a lot of sense. Sanders admitted that the plan is costly — and he wants Wall Street to pay for it. “Now, some people say that this legislation is expensive, and they’re right. It is,” he said. “Well, I’ll tell you how we’re going to pay for it. We are going to ask Wall Street to end their speculation. We’re going to put a speculation tax on Wall Street.”

This so called “speculation tax” or “speculation fee” will impact every working person who has a 401(k), IRA or any other type of investment. This will not impact the rich, but lower and middle income Americans who are trying to save for their futures. According to USA Today, the estimated cost of the program is $47 billion per year. That would cover, Sanders estimates, 67 percent of the $70 billion it costs for tuition at public colleges and universities. He proposes that states would cover the remaining 33 percent. This could lead to additional state income tax, fees and expense that would impact everyone.

“Free” Health Care Isn’t Free, Either

The single-payer health-care system that Bernie Sanders and others advocate would shift payment for all health care services to the federal government, eliminate private health insurance plans and dump all Americans onto public health care coverage. One estimate predicts that the scheme will most certainly include a massive payroll tax hike, an additional 4 percent personal income tax on all Americans and at least an 8 percent tax hike on businesses (even the small ones). The plan would cost, by a conservative estimate, at minimum, $16 trillion to sustain, just for the next decade. This could mean giving everyone Medicare or a new health-care system.

And Neither is “Free” Income

Universal basic income (UBI) is a policy that guarantees a fixed, unconditional income to all members of a designated group or entire country. For centuries, thinkers from Thomas Paine to Milton Friedman have kicked this concept around. Proponents claim UBI would be an efficient replacement for the United States’ expensive entitlement programs and, as a result, would actually reduce overall costs.

The reality is that UBI would just replace one pricey system for another. And unlike the current entitlement/welfare program, which has standards for determining who qualifies for certain aid, UBI would be given to everyone. This would dramatically increase the pool of citizens receiving benefits from the state and inflict massive expenses across the board. As mentioned, this would also create a disincentive for working, as we have seen in places like Greece. There are always claims that UBI could decrease, reform or even abolish our welfare system. But no one seems to have any idea about how this transition would actually look.

The likely scenario is that UBI would be in addition to, not instead of, the current welfare program. The idea of changing Social Security is known as the “third rail of politics” because the mere mention of it can mean political death. Anyone in the policy realm knows that there is no better way to alienate older constituents than by threatening to take away their Social Security benefits. In fact, the mere mention of decreases usually causes rooms full of senior citizens to fear for their well-being. Even if an alternative plan is presented to them, it does not calm their fears of what might happen during the transitionary period.

Also, trying to get individuals transitioned off of one welfare plan and into the next requires, at least temporarily, the funding of both programs. A decision to enact UBI would not magically abolish the American welfare system. America’s welfare program has been around for so long, it would take time to unroot it. Too many people have become reliant on our welfare state to have it simply wiped out overnight.

And who is going to pay for the process in the meantime? Well, any working American! At some point it no longer makes sense to work when you can simply get ‘free’ income from the government.

If anything, incorporating UBI in America would most likely result in an additional layer of welfare being added on top of our existing programs. This would, in effect, increase the state’s power rather than decrease it. Governments are rarely keen on relinquishing their power, and there is great power in controlling the welfare of the citizenry. It is therefore highly unlikely that the welfare state as we know it today would simply cease to exist.

UBI creates the illusion of decreasing the welfare state, when the facts of the matter all point to the contrary. Everyone would like to live in a society where no one wants for anything and everyone is provided for. But we live in a society of individuals with individual aspirations and goals. Pretending that we can centrally plan a welfare system with so many distinct wants and needs is unrealistic and unobtainable.

Socialism Is a Focus for the 2020 Election

The push for socialist policy is becoming more mainstream and will be a focus of the 2020 presidential election.

On March 18, 2019, Democratic 2020 presidential candidate Andrew Yang reiterated on MSNBC his proposal to give every American universal basic income each month — $1,000 per month for doing nothing — by taxing tech giants such as Amazon and Google. “It’s about 1.8 trillion a year past current expenses,” he said, before pointing out that Amazon paid “zero” taxes last year. Yang went on to state, “Amazon’s sucking up $20 billion in business every year, putting 30 percent of American malls out of business. We need to pass a value-added tax that would get the American people a slice of every Amazon transaction, every Google search, every robot truck mile.”

What he doesn’t state is how many jobs the tech giants have created and how they in fact help lower- and middle-income people by providing lower-cost goods and services. The problem is that socialism doesn’t work. It ultimately hurts the most vulnerable in our society while enriching a few elites at the top. Perhaps this is what those politicians proposing socialist policy want.

During his 2016 bid for the presidency, Bernie Sanders really moved the socialist agenda to the mainstream. Sanders presents socialism as just a generous social safety net. This narrative says government is a benevolent caretaker and pays for everybody’s needs by taking from the very rich to help the poor and the middle class.

Ironically, when you start to dig a little deeper, many who claim to support socialism do not actually like the true definition of it — the idea of government running businesses. If socialism is framed as government running Uber, Amazon, Facebook, Google, Apple, etc., it does not go over well. The Reason-Rupe study mentioned earlier notes that millennial preferences might not be so different from older generations, once terms are defined.

Socialism Has a Poor Track Record

In my opinion, we must move away from labels and perceptions and look at the facts. We have seen over and over that a centralized or socialist economy doesn’t work. It takes away the incentive for individuals to grow and leads to high unemployment and lower standards of living.

Stephen Moore, the Distinguished Visiting Fellow for Project for Economic Growth at The Heritage Foundation, takes it even further. He noted in 2015 that “Greece was about to slide into fiscal oblivion. This is the natural and unavoidable consequence of socialism everywhere it has been tried. Financial collapse.”

History has proven that that lower tax rates and less government regulation will lead to more economic prosperity and lower unemployment. Capitalism and a free economy lead to higher employment and more opportunities for all. Paying a guaranteed income to everyone will disincentivize many from working.

As taxes rise and there is no incentive to grow business, productivity drops. As productivity drops, revenue to the government drops, and more taxes must be levied. Ultimately economies collapse, while unemployment and poverty rise. History has repeated itself many times in this regard. Whether it’s the USSR, China, Cuba, Vietnam, the former East Germany, North Korea, Laos, Nicaragua, Zimbabwe, Cambodia, Venezuela or any of the other failed experiments in socialism, it has never worked anywhere.

On May 17, 2018, Investor’s Business Daily stated, “There has never been a successful socialist government in history. None. Everywhere socialist precepts are put in place, poverty, loss of freedom and rights, and societal decline inevitably follow. Collapse is a frequent result… It has led only to misery, deprivation, government control and a loss of basic human rights. Socialist regimes always start off with high ideals, promising ‘free’ this, and ‘free’ that — education, health care, whatever. But as their ideas fail, they inevitably resort to compulsion, and eventually torture, political ‘re-education,’ imprisonment, exile and murder for those who disagree.”

Let’s look at just a few examples of countries in which socialist policies have been enacted.

1. Cuba

Cuba is one of the most prominent socialist nations, having a mostly state-run economy, a national health-care program, government-paid (free) education at all levels, subsidized housing, utilities, entertainment and even subsidized food programs. These subsidies compensate for the low salaries of Cuban workers. According to Cuba’s National Office of Statistics, wages in Cuba averaged just 494.4 pesos ($18.66) monthly from 2008 to 2015. Compare that figure with income in the United States. The median U.S. household income in 2017 was $61,372 per year, or $5,114.33 per month.

2. Greece

Unemployment— youth unemployment in particular — remains one of the biggest struggles in Greece. In 2016, 47.3 percent of the Greek population under age 25 was out of work. That’s nearly half the population and more than two times the average rate across the euro zone. This situation is largely the result of large government pensions and benefits and declining tax revenue. Ironically, lower taxes on the wealthy generally increase tax revenue.

3. Sweden

From 1970 to 1991, Sweden’s socialist government attempted socialism, and it failed dismally. In fact, Sweden recorded the lowest growth rate in Western Europe. After 1991, the government introduced market reform, tax cuts and welfare cuts. Those changes resulted in massive growth, allowing the country to have the second-highest growth rate in Europe, with only the UK being higher during this period.

4. Venezuela

The International Monetary Fund predicted that by the end of 2018, the annual inflation rate in Venezuela would reach 1 million percent. That means that a candy bar that cost $1 today would cost $10,000 at the end of the year. An article in The Washington Post explains why hyperinflations like those in Venezuela occur:

The government wants to spend much more money than it is collecting in taxes — so much more that no one is willing to lend it the money to cover the deficit. Instead, the government uses the central bank to finance the deficit. That puts more money in the economy, but since it’s chasing the same number of goods and services, prices rise to soak up all the extra cash. Unless the government manages to close its budget deficit, it must print even more money to buy the same amount of stuff.

The article goes on to say that Venezuelan president Nicolás Maduro stays on this destructive path while the country’s citizens starve because of socialism.

This is not an issue of left vs. right or of Democrat vs. Republican. This is an American issue. The rise in popularity of socialism in the United States should be a concern to all of us. Just how far have Americans leaned toward socialism? According to a 2017 survey of adults by the American Culture and Faith Institute (ACFI), 40 percent of adults said they preferred socialism to capitalism. That is alarming! I believe the people in this camp need to review what history has told us about socialism’s repeated failure and to understand what socialism really is.

Why Socialism Doesn’t Work

So why does socialism fail again and again? Mark J. Perry, Ph.D., a scholar at the American Enterprise Institute and a professor of economics and finance at the University of Michigan’s Flint campus, gives this reason:

Socialism does not work because it is not consistent with fundamental principles of human behavior. The failure of socialism in countries around the world can be traced to one critical defect: it is a system that ignores incentives. In a capitalist economy, incentives are of the utmost importance. Market prices, the profit-and-loss system of accounting and private property rights provide an efficient, interrelated system of incentives to guide and direct economic behavior. A centrally planned economy without market prices or profits, where property is owned by the state, is a system without an effective incentive mechanism to direct economic activity. By failing to emphasize incentives, socialism is a theory inconsistent with human nature and is therefore doomed to fail.

As we write this in April 2019, we are seeing one of the strongest economies in history for the United States, with record employment, rising wages, strong corporate profits and rising markets. This is the result of less tax, less government regulation and more free markets. This benefits everyone, especially lower- and middle-income Americans. This economic prosperity is good news, especially for today’s younger generations to succeed.

We have an amazing opportunity to benefit all Americans with good jobs and a strong economy. Some of the people who are in favor of socialist policies have the best intentions. But it simply doesn’t matter if those espousing free wages and free college are doing so for their own political gains or because they believe it will benefit someone. What matters is that these policies can cripple our economy and country. This is not a political opinion but an economic fact. As we approach the 2020 elections, it is important to consider and support candidates whose economic and social policies will benefit the country — regardless of party affiliation.

Why Capitalism Does Work

Capitalism is not fair, and that’s why it works. Capitalism creates the incentive to innovate and work hard to be rewarded, which leads to more jobs and a better economy for all. We must get away from semantics, politics and labels and focus on the real problems that these “free programs” address. In many ways, creating jobs, through lower taxes and less government intervention does, solves the issues. People can pay off debts (college loans or otherwise), afford housing and food, and receive quality health care and health insurance.

Nobody knows what the future holds. But regardless of the new political and economic policy, world events or changes that come, we are here for you. Rather than planning based on speculation, we believe in planning based on your needs and current facts. Our customized and proactive approach allows you to adapt to any changes in our tax laws, markets or economy.

We look forward to being your partner. Please contact us whenever we may be of service to you, your family and friends. Right now, we are taking clients only by referral. We are happy to meet, without cost or obligation, with anyone you feel would benefit from our personal Vision Planning™ process.

__________

This information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of the professionals at Carver Financial Services, Inc., and not necessarily those of Raymond James. Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members.

March 2019

Barron’s Names Randy Carver To It’s Top 1200 Financial Advisor List for 2019

March 11, 2019 – Barron’s Magazine again named Randy Carver as one of the top advisors in the Nation and one of Ohio’s ten best financial advisors. Randy has been recognized by Barron’s each year since 2008.

Rankings are based on data provided by the nation’s 4,000 most productive advisors. Factors included in the rankings: assets under management, revenue produced for the firm, regulatory record, quality of practice and philanthropic work. Investment performance isn’t an explicit component because not all advisors have audited results and because performance figures often are influenced more by clients’ risk tolerance than by an advisor’s investment-picking abilities. Barron’s listed their top 1,200 putting Randy in the top 4/10th of 1% of all advisors.

To see full listing click here.

Carver Financial Services Inc. is an independent firm. Raymond James is not affiliated with Barron’s. Neither Raymond James nor any of its Financial Advisors have paid a fee in exchange for this recognition. This recognition is not indicative of future investment performance, is not an endorsement, and may not be representative of individual clients’ experience.

{kind=link}